.png?ext=.png)

On 12 January 2024, the Australian Government released the exposure draft legislation Treasury Laws Amendment Bill 2024: Climate-related financial disclosure to amend parts of the Australian Securities and Investment Commission Act 2001 (Cth) and the Corporations Act 2001 (Cth). The subsequent Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 was introduced into Parliament on 27 March 2024.

Schedule 4 requires certain large businesses to prepare an annual sustainability report and disclose their climate risks and opportunities in accordance with the new Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information (AASB standards) created by the Australian Accounting Standards Board. The new standards will align with the International Financial Reporting Standards S1 and S2 released by the International Sustainability Standards Board and are expected to be finalised by the end of 2024.

The new framework intends to replace the variety of climate disclosure guidelines and standards currently available for Australian businesses (each with their own distinct reporting requirements and styles) with one standardised, internationally aligned reporting framework. This will promote consistent and comparable reporting of climate-related financial information.

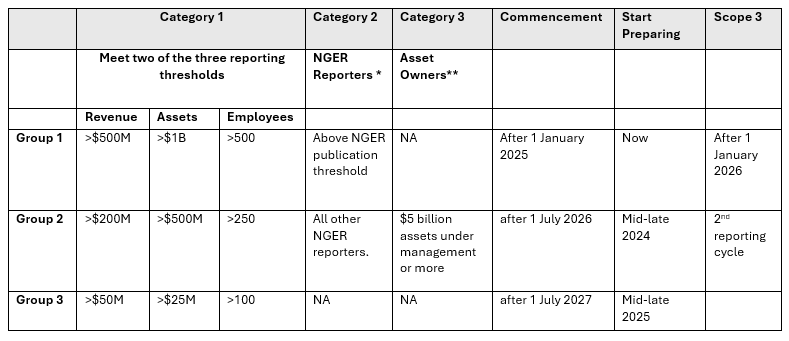

Businesses that are required to lodge climate-related financial reports under Chapter 2M of the Corporations Act 2001 and fall within one or more of the three categories in the table below, will be classified as a reporting entity as one of three groups specified in the table.

* National Greenhouse and Energy Reporting (NGER) Reporters (Entities with emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (Cth)

** (Asset owners with assets of $5 billion or more (including the entities they control).

The reporting requirements will be phased in over time, with the largest businesses (Group 1) to commence reporting in 2025, and Groups 2 and 3 to follow in July 2026 and July 2027 respectively.

Importantly, Scope 1 and 2 greenhouse gas emissions must be reported in the first year, while Scope 3 emissions will need to be disclosed starting in the second year of reporting. Scope 3 emissions are indirect emissions (not included in Scope 2 greenhouse gas emissions) that occur in the value chain of the reporting company, including upstream and downstream emissions. These emissions contribute the majority of corporate emissions and, if addressed, can lead to significant opportunities for improvement for the business.

Many organisations identify their Scope 3 emissions using the 15 categories defined in the Greenhouse Gas Protocol – Corporate Value Chain (Scope 3) Accounting and Reporting Standard and use calculation methods within the GHG Protocol Scope 3 Calculation Guidance. The GHG Protocol is the most widely used method for companies to account for these types of value chain emissions. In Australia, the new AASB standards align with the GHG Protocol and provides the 15 categories as examples that a company could consider when measuring its Scope 3.

Other organisations are developing their own method for calculating Scope 3 emissions to address unique challenges of specific industries. For example, the Green Building Council of Australia has released a Scope 3 Emissions Discussion Paper for the real estate sector, and Lend Lease has developed the Scope 3 Emissions Protocol. This protocol outlines the categories of Scope 3 emissions relevant to their value chain and sets targets for reducing these emissions as part of their broader goal of achieving Absolute Zero Carbon by 2040.

Although a smaller business within the steel value chain may not fall into Group 1, 2, or 3 under the new Act, if it supplies to a larger business classified as a reporting entity, it could still be included under the Scope 3 requirements. Consequently, the smaller business may need to address its future emission reporting obligations as a supplier.

Whilst the reporting framework is still being finalised, the ASI is working alongside key industry stakeholders to assist its members in keeping up to date with reporting requirements in this evolving space. The ASI has been advocating key support needs pertinent to our industry in relation to Climate Related reporting with the Commonwealth Government, which includes the need for a roll out of education and awareness programs nationally, provision of support tools, relevant training initiatives for our people working on such reports, and the expected future requirement of skilled auditors and advisors.

The ASI’s Steel Sustainability Australia scheme was developed specifically for the steel supply chain and is one mechanism businesses can use to determine and track its Scope 1 and 2 emissions to prepare for the up-coming mandatory reporting requirements.

If you would like more information on SSA please contact the SSA Scheme Manager Melinda Coles on ssa@steel.org.au.