ASI members are reporting that they are being very significantly undercut by imported fabricated goods priced at between 15% and 50% lower than the cheapest local offer. This issue is particularly impacting East Coast fabrication businesses that are reliant on the portal frame market for structural steel, but it is also having a detrimental effect on a wide range of other steel product manufacturers. The impacted businesses are reporting loss of viability due to decreased profit margin, loss of revenue due to lower volumes and capacity utilisation, and increased costs. Nearly half of those surveyed are undertaking some form of restructuring in an attempt to remain viable. The brunt of the impact is being born by small and medium sized businesses, each typically employing between 20 and 200 Australians, and providing skilled employment in their local region.

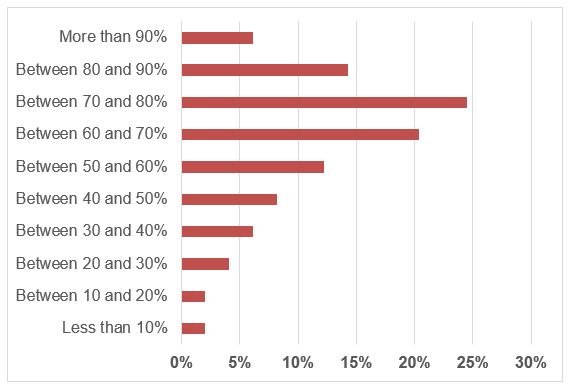

Approximately 80% of those surveyed reported that they are now operating at less than 80% capacity utilisation, which is typically a benchmark for breakeven profitability in manufacturing. At the extremely distressed end of the response, one fifth of businesses responded that they are operating at below 50% of production capacity.

The survey adds considerable additional information to the reports provided to the ASI by individual member businesses over the last 12 months. Members have described a grim picture of needing to lay off long term, skilled staff members in order to remain viable in the face of greatly diminished order books.

The extent of the price undercutting being reported is indicative of subsidies from the country of origin, and/or dumping being a major contributor to the problem. The use of subsidies and dumping of goods as a means to gain market share are both unfair, and illegal. This is because local businesses are not able to viably compete with international competitors that benefit from a range of subsidies.

The ASI is engaging with state and federal governments in order to bring this problem to their attention, explain the damage that is being done to strategically important local industries, and to identify what courses of action are available to provide relief to members.

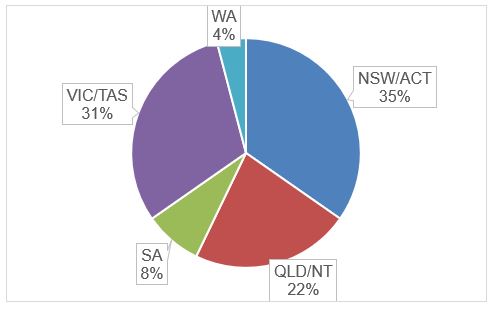

The majority of survey respondents were from New South Wales, Victoria, and Queensland.

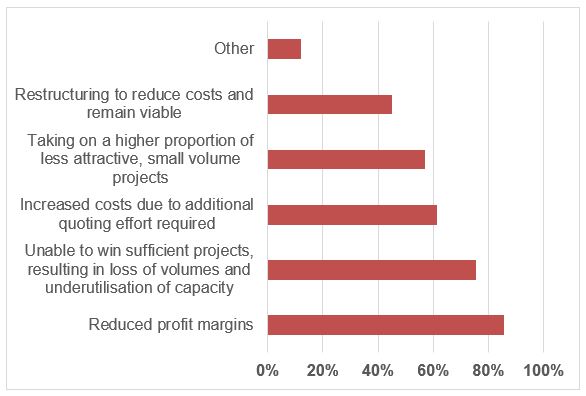

Nearly all respondents have reported reduced profit margins as a consequence of imported products, and most are operating at greatly reduced capacity utilisation. The loss of opportunity to work on large, more efficient projects has led to the need to focus on smaller, less attractive jobs, and/or reduce staffing to reduce costs.

The steel fabrication and manufacturing industry is capital intensive, with significant overhead costs. Therefore, it is essential for capacity utilisation to be at or above 80% in order to remain profitable. The large proportion of businesses operating well below this benchmark is indicative of the seriousness of the problem.

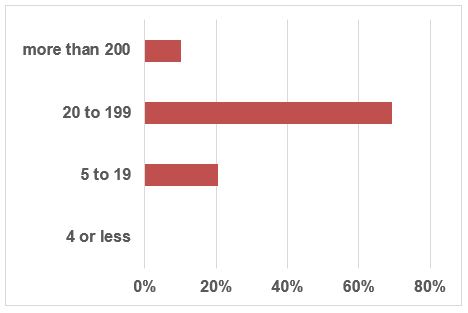

The great majority of businesses impacted are small and medium sized enterprises or SMEs.

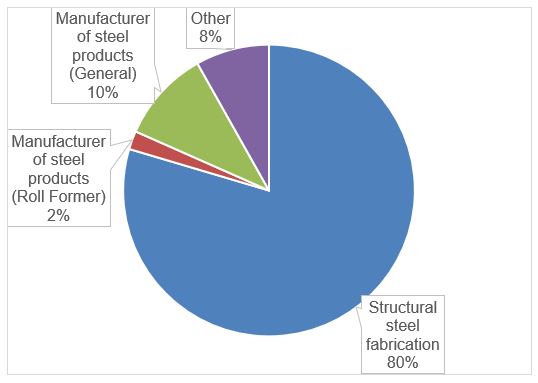

The issue of very low-priced imported fabricated goods is largely impacting structural steel fabrication, with selected steel product manufacturers also affected.

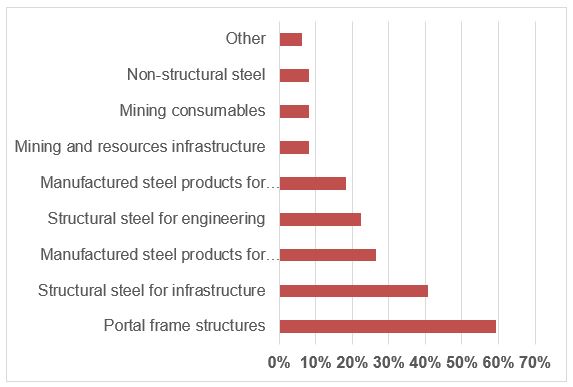

Businesses reliant on the portal frame market are the most impacted.

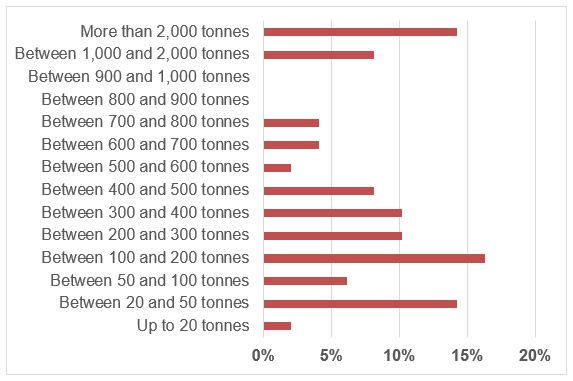

The issue is impacting businesses across the spectrum of production capacity.

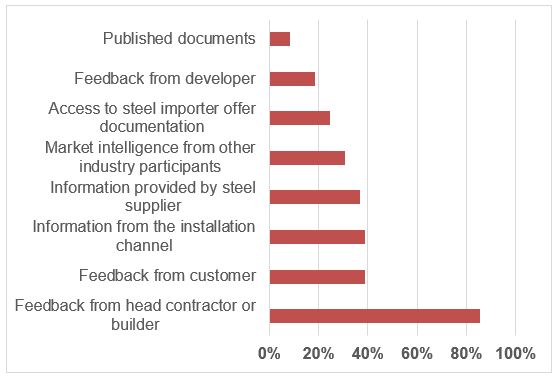

Members are drawing on a wide range of sources for their information, which supports the credibility of responses provided.